Industry Trends, Compliance Shifts, and Deal Activity Shaping Mid-Market Process Manufacturers

📚 New Blog Posts

1. Morehouse Foods Gains Real-Time Visibility and Recall-Ready Traceability with BatchMaster Web ERP

2. From Blueprint to Business Control: Solution Design & Execution Readiness in ERP Implementation

3. From Operational Silos to a Unified Platform: How Florida Nutrition Scaled with BatchMaster ERP

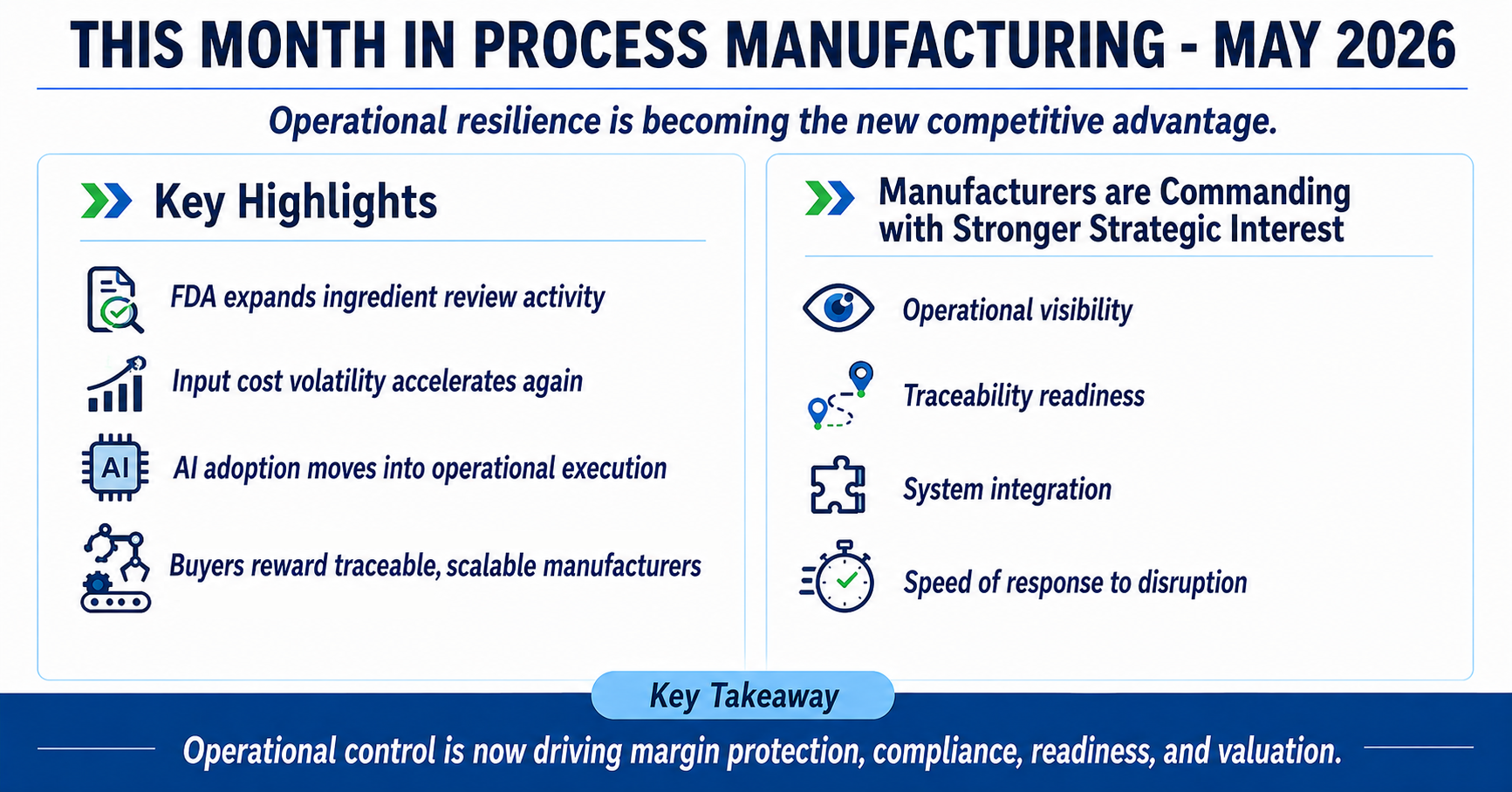

The Brief

May reinforced a structural shift across process manufacturing: operational resilience is now being pressured by tightening compliance requirements, volatile input costs, and execution gaps. FDA ingredient review activity accelerated, energy-driven costs rose again, and AI discussions moved beyond experimentation toward operational integration.

Also, M&A activity continued to favor manufacturers with scalable infrastructure, traceable operations, and stronger operational control. For $5M–$200M manufacturers, maintaining visibility and control is becoming just as important as growth.

Compliance & Regulatory Watch

MAHA & Ingredient Policy: FDA Expands Post-Market Chemical Review Activity

May marked another escalation in FDA’s broader Human Foods Program activity under the MAHA framework, but the signal this month was more operational than political: the FDA is moving from broad policy direction toward formalized review mechanisms and enforcement structure.

FDA Action (May 2026)

In May, the FDA finalized its Enhanced Systematic Process for Post-Market Assessment of Chemicals in Food, formally outlining how the agency will prioritize and reassess chemicals already present in the food supply. At the same time, the FDA issued Requests for Information (RFIs) on BHT (Butylated Hydroxytoluene) and Azodicarbonamide (ADA), expanding beyond the earlier BHA reassessment launched in February. (Covington)

Input cost volatility accelerated again

- GRAS reform is moving closer to mandatory notification expectations

- Post-market chemical reassessments are becoming systematic rather than isolated

- Ingredient reviews are increasingly tied to broader labeling and consumer transparency initiatives

This is no longer a theoretical regulatory shift. The FDA is now building repeatable infrastructure for continuous ingredient oversight.

Ingredients Under Heightened Scrutiny

May’s review activity centered around several ingredient categories already under pressure across retail and regulatory channels:

BHA and BHT (synthetic preservatives)

- Azodicarbonamide (ADA) used in baked goods and dough conditioning

- Artificial food colors under expanded “no artificial colors” positioning

- Phthalates and indirect food-contact chemicals

- GRAS self-affirmed substances lacking formal FDA review

The implication for manufacturers is operational, not symbolic.

Ingredients that were historically treated as “accepted legacy inputs” are increasingly becoming formulation liabilities, particularly for companies selling into retailer-driven or consumer-sensitive channels.

State-Level Complexity Continues Expanding

California continues leading additive and food chemical enforcement momentum, while broader state-level discussions around additive restrictions and labeling authority continue expanding across multiple jurisdictions.

The result for manufacturers operating nationally is growing formulation fragmentation:

- Regional labeling inconsistencies

- Increased SKU variation risk

- More complex supplier qualification requirements

- Expanded documentation burdens for formulation changes

Manufacturers are increasingly being forced to manage multiple compliance realities simultaneously rather than one national standard.

Operational & Financial Impact

The cost impact of these regulatory shifts is becoming increasingly measurable:

- Reformulation projects are accelerating

- Ingredient sourcing flexibility is narrowing

- Validation and testing cycles are becoming more frequent

Retailer-driven compliance expectations are out-pacing formal enforcement timelines.

Most importantly, ingredient governance is becoming a systems issue rather than an R&D issue.

Manufacturers that lack integrated formulation, quality, supplier, and traceability visibility will struggle to respond quickly enough as review cycles shorten.

The operating environment is shifting from:

“Can we comply?” → “How quickly can we adapt?”

1. FSMA 204: Preparation Window Is Becoming an Execution Window

Status:

Compliance date remains extended to July 2028.

Applies to:

Food manufacturers handling items on the Food Traceability List (FTL).

Although the formal deadline remains years away, May showed increasing industry focus on operational readiness rather than regulatory timing.

What’s changing operationally:

- Greater emphasis on event-level traceability

- Faster recall-response expectations

- Increased retailer pressure for traceability visibility before enforcement begins

→ Operational impact: The biggest challenge is no longer collecting data. It is creating connected, usable visibility across operations.

Manufacturers still relying on spreadsheets or disconnected systems are discovering that traceability gaps are often created between departments rather than inside them.

2. GMP & Batch Record Enforcement Signals Continue Intensifying

Applies to:

Food, beverage, and nutraceutical manufacturers.

Inspection trends in 2026 continue emphasizing:

- Batch record completeness

- Deviation documentation

- Electronic record integrity

- Validation of process adherence

→ Operational impact: Manual batch documentation is increasingly becoming difficult to defend during audits. Regulators are placing greater focus on:

- Timestamp accuracy

- Record accessibility

- Traceable production changes

- Alignment between production activity and quality documentation

The expectation is shifting from:

“Records exist” → “Records prove operational control.”

3. 21 CFR Part 11: System Validation Pressure Is Increasing

Applies to:

Manufacturers use electronic records and signatures.

As manufacturers accelerate digital adoption, regulators are placing greater attention on:

- System validation

- Secure audit trails

- Tamper-evident records

- Cross-functional data consistency

→ Operational impact: Disconnected operational systems are increasingly creating compliance risk.

The challenge is no longer digitization itself. It is proving that systems are reliable, validated, and synchronized across production, quality, and compliance functions.

Signal 1: Input Cost Volatility Accelerated Again

What happened:

The ISM Manufacturing Prices Paid Index surged to 84.6 in April 2026, its highest level in four years, driven heavily by energy market disruption and rising geopolitical instability linked to Middle East LNG and fuel supply pressure.

Manufacturing implication:

Input volatility is no longer behaving like traditional inflation cycles.

Energy markets, freight exposure, and supplier instability are now creating rapid swings in:

- Utility costs

- Feedstock pricing

- Ingredient sourcing economics

- Production planning assumptions

Static costing models are becoming increasingly unreliable in fast-moving operational environments.

Before your next leadership meeting, ask:

If input costs spike another 10–15% in one quarter, how quickly can we identify margin exposure at the SKU level?

Signal 2: AI Adoption Is Moving into the Organizational Design Phase

What happened:

Recent manufacturing studies showed that AI adoption challenges are no longer primarily technology related. They are increasingly tied to leadership structure, workflow redesign, and frontline integration.

Manufacturing implication:

Many manufacturers have moved past experimentation but remain stuck between pilot programs and scalable operational deployment.

The core problem is becoming clearer:

AI cannot improve operational execution if workflows, accountability structures, and plant-level decision-making remain unchanged.

Before your next leadership meeting, ask:

Are we implementing AI tools, or redesigning how operational decisions actually get made?

Signal 3: Manufacturing Capability Is Becoming a Valuation Asset

What happened:

Private equity and strategic buyers continued prioritizing smaller, capability-driven manufacturing acquisitions, especially in specialty chemicals, ingredient processing, and regulated manufacturing environments.

Manufacturing implication:

Domestic production capability, traceability maturity, and operational integration are increasingly being treated as strategic assets rather than operational overhead.

Manufacturers with:

- Complex formulation capability

- Strong documentation systems

- Integrated operational visibility

are commanding stronger strategic interest even without hypergrowth narratives.

Before your next leadership meeting, ask:

If a buyer evaluated our operations today, would they see operational leverage or operational risk?

M&A Intelligence

- $190M acquisition (transaction value): Ecovyst acquired Calabrian sulfur derivatives business from INEOS (Specialty Chemical)

Ecovyst signed a definitive agreement to acquire INEOS Enterprises’ Calabrian sulfur dioxide and sulfur derivatives business for approximately $190M. The acquisition expands Ecovyst’s manufacturing footprint across sulfur-based specialty chemicals used in water treatment, mining, and industrial processing.

Signal: Buyers are actively expanding into highly specialized chemical production categories where domestic manufacturing capability and process expertise create long-term supply chain leverage.

- $95M acquisition (transaction value): Turpaz Industries acquired Phoenix Flavors & Fragrances (Food Ingredients / Flavor Manufacturing)

Turpaz Industries acquired U.S.-based Phoenix Flavors & Fragrances for $95M, adding formulation expertise, flavor extraction capabilities, and a full-scale U.S. operational platform serving food and beverage manufacturers.

Signal: Ingredient and formulation manufacturers with specialized IP and scalable production infrastructure continue attracting premium strategic interest, particularly in clean-label and flavor innovation markets.

- Strategic platform expansion: Praana Group acquired Multi-Chem (Specialty Chemical / Energy Chemicals)

Praana Group completed the acquisition of Multi-Chem under its Sterling Specialty Chemicals platform, combining specialty polymer and surfactant manufacturing with oilfield chemical application expertise across upstream and downstream energy operations.

Signal: Manufacturing buyers are increasingly pursuing integrated operating platforms that combine production capability with technical service and application-level expertise.

Valuation Signal

May’s deal activity reinforced a clear trend across process manufacturing: buyers are paying premiums for operational defensibility. Manufacturers with specialized formulation capabilities, domestic infrastructure, traceable operations, and strong quality systems continue attracting stronger valuation interest.

Meanwhile, generalized manufacturing capacity without differentiated operational capability is becoming less attractive, widening the valuation gap between capacity providers and capability-driven manufacturers.

Final Takeaway

May’s signals reinforced a broader reality across process manufacturing: competitive advantage is shifting away from scale alone and toward operational resilience. Ingredient scrutiny is accelerating, cost assumptions remain unstable, compliance expectations are tightening, and operational execution gaps are becoming more visible.

The manufacturers positioned strongest for the next cycle will be the ones that adapt faster, maintain stronger operational control, connect systems effectively, and respond to disruption without losing visibility. In process manufacturing, operational control is no longer just an efficiency advantage. It is becoming the foundation of margin protection, compliance readiness, and enterprise value.

Resources & Sources

MAHA & Ingredient Policy

- FDA Finalizes Food Chemical Safety Post-Market Assessment Program, Launches Reassessment of BHT & ADA (U.S. Food and Drug Administration)

- FDA Launches Assessment of BHA, a Common Food Chemical Preservative (U.S. Food and Drug Administration)

- FDA Systematic Process for Ensuring the Post-Market Safety of Chemicals in Food (U.S. Food and Drug Administration)

- FDA List of Select Chemicals in the Food Supply Under Review (U.S. Food and Drug Administration)

- FoodNavigator — FDA Takes Aim at BHT and ADA in New Food Chemical Safety Program (FoodNavigator.com)

- Reuters — FDA to Review Decades-Old Food Preservative in Safety Overhaul (Reuters)

Compliance & Regulatory

- FDA Human Foods Program — Post-Market Food Chemical Safety Framework (U.S. Food and Drug Administration)

- FDA Chemical Review Work Plan & Ongoing Assessments (U.S. Food and Drug Administration)

- FDA BHT & ADA Requests for Information (RFI) (U.S. Food and Drug Administration)

Industry Signals

- Trading Economics — ISM Manufacturing Prices Paid Index (Trading Economics)

- Reuters — US Manufacturing Sector Holds Steady; Input Costs Hit Four-Year High (Reuters)

- Manufacturing Dive — Frontline Leaders Are Crucial for Adopting AI (Manufacturing Dive)

- 2026 Roadmap on AI & Machine Learning for Smart Manufacturing (arXiv)

- Wall Street Journal — ISM Manufacturing Survey Shows Rising Price Pressures (Wall Street Journal)

M&A Resources & Sources

Ecovyst → Calabrian Sulfur Derivatives Business

- Ecovyst Acquisition Announcement

- Specialty Chemicals Industry Coverage

Turpaz Industries → Phoenix Flavors & Fragrances

- Turpaz Acquisition Coverage

Praana Group → Multi-Chem

- Praana Group Acquisition Announcement

- Additional Transaction Coverage

Market & Valuation Trend References

- Kroll Food & Beverage M&A Insights Spring 2026

- Food & Beverage M&A Market Discussion