📚 New Blog Posts

1. Why “95% Inventory Accuracy” Still Fails Process Manufacturers

3. How a $20 Million Paint & Coatings Manufacturer Finally Saw Where It Was Making Money

A monthly update for process manufacturing leaders across food, pharmaceutical, nutraceutical, chemical, and personal care industries

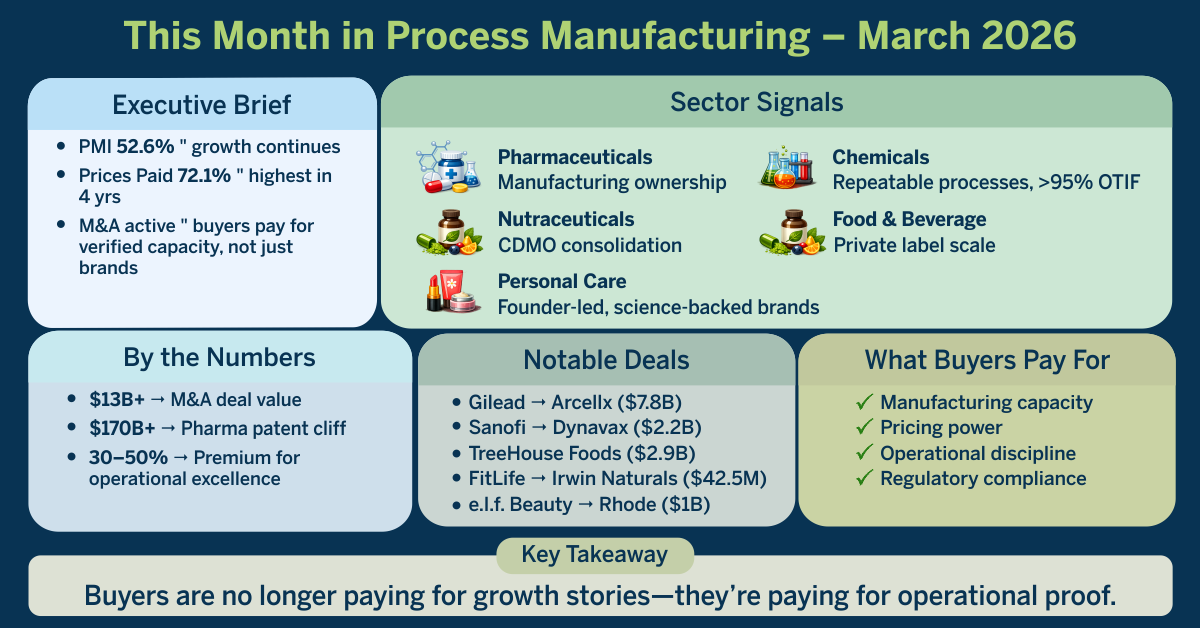

🎯 EXECUTIVE BRIEF

March 2026 is shaping up as a pivotal month for mid-market process manufacturers ($5M–$50M revenue). Inflation continues to climb while M&A activity remains aggressive. The ISM Prices Paid Index surged to 72.1%, the highest level in nearly four years, reflecting rising raw material costs and global supply chain pressures.

Yet buyers remain active. Gilead paid $7.8B for Arcellx CAR-T manufacturing, while TreeHouse Foods—the largest US private-label manufacturer—went private for $2.9B. The message is clear: buyers are paying for verified manufacturing capacity and operational control, not just products or brands.

Companies with documented pricing power, robust margin stability, and operational discipline continue to command premium valuations despite macroeconomic pressures.

📊 BY THE NUMBERS

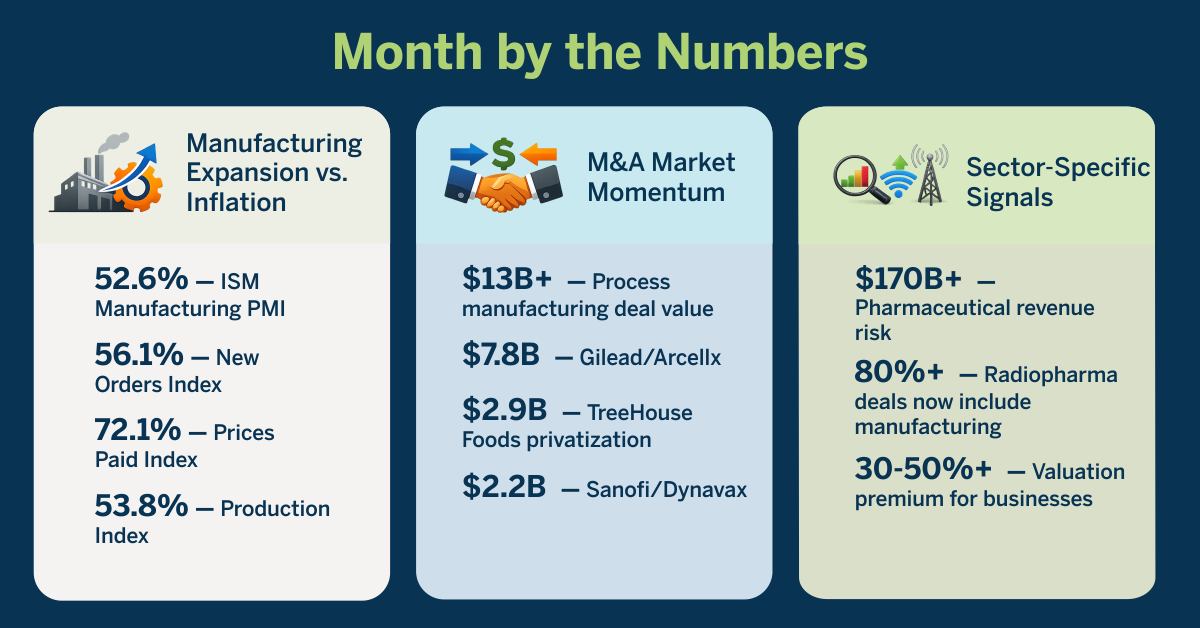

Manufacturing Expansion vs. Inflation

- 52.6% — ISM Manufacturing PMI (Purchasing Managers’ Index)

- 56.1% — New Orders Index (slightly up)

- 72.1% — Prices Paid Index (highest in nearly 4 years)

- 53.8% — Production Index (modest growth)

M&A Market Momentum

- $13B+ — Process manufacturing deal value in February 2026

- $7.8B — Gilead/Arcellx (CAR-T therapy)

- $2.9B — TreeHouse Foods privatization

- $2.2B — Sanofi/Dynavax (adult vaccines)

Sector-Specific Signals

- $170B+ — Pharmaceutical patent cliff revenue at risk by 2032

- 80%+ — Radiopharma deals now include manufacturing or isotope integration

- 30–50% — Valuation premium for businesses with documented operational excellence

Implication: Manufacturing growth continues, but cost management and verified operational control are now critical for capturing buyer premiums.

🏭 MARCH 2026 PROCESS MANUFACTURING INSIGHTS

Pharmaceutical & Life Sciences

- Patent cliff pressure and vertical integration accelerate acquisitions.

- Gilead/Arcellx ($7.8B) demonstrates buyers prioritizing manufacturing ownership over licensing.

- Sanofi/Dynavax ($2.2B) reinforces the vaccine manufacturing capacity trend.

- Siegfried/Noramco acquisition highlights the scarcity of US-based large-scale custom pharma sites.

- 80%+ of radiopharma deals now include operational or isotope integration.

Buyer Focus: US-based manufacturing, vertical integration, next-gen platforms, and late-stage clinical assets.

Chemical Manufacturing (Specialty & Coatings)

- Sector expansion persists despite raw material and tariff pressures.

- PE and strategic buyers focus on repeatable formulations, operational discipline (>95% OTIF, <5% deviation), and US production assets.

- Specialty chemical consolidation continues; EBITDA multiples remain high (5.5–6.5x) for integration-ready businesses.

Buyer Focus: Operational discipline, capacity control, pricing power.

Nutraceutical & Supplement Manufacturing

- Contract manufacturing consolidation accelerates.

- Metagenics/Symprove and FitLife/Irwin Naturals ($42.5M) reinforce CDMO consolidation.

- AI-driven discovery and third-party certifications (NSF, USP, ConsumerLab) are now standard requirements.

Buyer Focus: Vertical integration, professional-grade formulations, recurring revenue, US manufacturing.

Food & Beverage Manufacturing

- Private label and contract manufacturing continue consolidating.

- TreeHouse Foods ($2.9B) and Refresco/SunOpta ($6.50/share) highlight scale and operational excellence premiums.

- Demand remains resilient; manufacturers with diversified customers and pricing power benefit most.

Buyer Focus: Scale, operational discipline, pricing mechanisms.

Personal Care & Cosmetics

- Strategic buyers continue selective acquisitions.

- e.l.f. Beauty/Rhode ($1B) and Unilever divestitures show premium for founder-led, science-backed brands.

- US manufacturing capabilities are increasingly valued amid tariffs and reshoring.

Buyer Focus: Founder-led, science-backed brands, US production, DTC performance metrics.

💸 NOTABLE DEALS — MARCH 2026

| Sector | Deal | Value | Insight |

| Pharmaceutical | Gilead → Arcellx | $7.8B | Vertical integration, CAR-T production |

| Pharmaceutical | Sanofi → Dynavax | $2.2B | Vaccine capacity acquisition |

| Pharmaceutical | Siegfried → Noramco | N/A | US manufacturing site premium |

| Food & Beverage | Investindustrial → TreeHouse | $2.9B | Platform consolidation, operational scale |

| Food & Beverage | Refresco → SunOpta | $6.50/share | Functional beverage expansion |

| Nutraceutical | Metagenics → Symprove | N/A | CDMO consolidation |

| Nutraceutical | FitLife → Irwin Naturals | $42.5M | Recurring revenue model |

| Personal Care | e.l.f. Beauty → Rhode | Up to $1B | Founder-led, DTC growth |

| Personal Care | Unilever → Rare Beauty | N/A | Portfolio optimization |

🎤 INDUSTRY VOICE

- Location Premium in M&A: New Jersey pharma site commanded 7.8x EBITDA, 60% above average, due to scarcity and regulatory licensing.

- Lesson Across Sectors: Geographic location and manufacturing capacity now drive premiums more than growth or customer base.

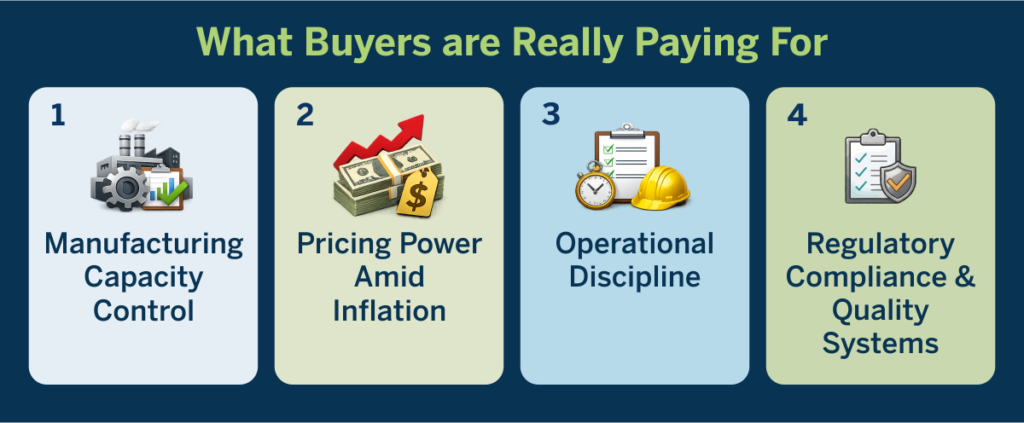

⚙️ WHAT BUYERS ARE REALLY PAYING FOR

- Manufacturing Capacity Control — US-based production, vertical integration, limited site availability drives 15–40% premium.

- Pricing Power Amid Inflation — Contract pass-throughs and documented mechanisms command 20–30% advantage.

- Operational Discipline — Complete batch records, OTIF >95%, deviation <5%, 30–50% valuation premium.

- Regulatory Compliance & Quality Systems — FDA, DEA, EPA, GMP compliance; incomplete documentation = 15–25% discount.

🔧 OPERATOR PLAYBOOK

- Finance Leaders: Document pricing power, analyze inflation impact, update forecasts, prepare board presentations.

- Operations Leaders: Audit batch records, optimize capacity, review supplier costs, minimize waste.

- Technology/IT Leaders: Ensure ERP compatibility, assess real-time cost tracking, and maintain DR/BC plans.

- R&D & Regulatory: Verify FSMA/DEA/USP/GMP compliance, update training, and maintain clinical validation records.

- Cross-Functional: Inflation response, M&A readiness, pricing power, geographic advantage.

📜 POLICY & COMPLIANCE PULSE

- Tariffs & Trade: US manufacturing location premiums 15–25% amid steel/aluminum cost pressures.

- FDA: Pre-Check Program, advanced manufacturing guidance, FSMA 204 traceability (July 2028).

- EPA: PFAS reporting, TSCA updates, emission compliance scrutiny.

- Implication: Proactive compliance drives premium valuations; incomplete compliance discounts 15–25%.

📅 UPCOMING EVENTS — Q2 2026

- AIChE Spring Meeting — March 29-April 2, New Orleans, LA

- SupplySide Connect NJ — April 14-15, Secaucus, NJ

- Food Safety Summit — May 11-14, Rosemont, IL

💡 ONE-MINUTE EXECUTIVE TALKING POINTS

- Prices Paid Index hits 72.1% — cost management top priority

- ISM PMI 52.6%, New Orders 56.1% — expansion continues

- Vertical integration accelerating — Gilead/Arcellx, Sanofi/Dynavax

- US location premium emerging — 15–25% valuation advantage

- Contract manufacturing consolidation — TreeHouse, FitLife/Irwin

- Patent cliff urgency — $170B+ pharma revenue at risk

- Pricing power premium — 20–30% valuation advantage

- Operational documentation critical — 30–50% premium

- Regulatory compliance — incomplete docs create 15–25% discounts

- Geographic scarcity matters — strategic asset in 2026 M&A

📞 CONNECT WITH US

Have insights to share? Email us at: news@batchmaster.com

Discuss your business impact: Connect with operational leaders on manufacturing excellence, M&A trends, and process optimization.

📚 SOURCES & REFERENCES

Economic & Manufacturing Data:

- ISM Manufacturing PMI Report — February 2026

- ISM Official Report

- NAM Q4 2025 Manufacturers’ Outlook Survey

- U.S. Federal Reserve – Industrial Production

M&A & Industry Intelligence:

- STAT News – Gilead to buy Arcellx

- C&EN – Siegfried to buy Noramco

- PR Newswire – TreeHouse Acquisition

- Food Navigator USA – TreeHouse sold

- Bain – Pharma M&A Report 2026

Regulatory & Compliance:

- U.S. FDA – Newsroom

- Food Safety Magazine – FSMA 204

- U.S. EPA – Newsreleases

Nutraceutical & Supplement Intelligence:

- PE Hub – Dietary Supplement Deals

- SEC Filing – FitLife Irwin Acquisition

- New Hope Network

- Nutritional Outlook

Beauty & Personal Care:

- SEC Filing – e.l.f. Rhode Acquisition

- Beauty Packaging – Beauty M&A 2025

Industry Associations:

- SOCMA

- AIChE

- Natural Products Association

- Personal Care Products Council