📚 New Blog Posts

1. Cloud-Powered Growth: How Cosmetix West Modernized for Global Scale

2. ERP Project Planning & Kickoff: The Foundation for Successful Implementation

3. How to Achieve FDA Audit Readiness in Process Manufacturing

Industry Trends, compliance shifts, and deal activity shaping growth-oriented process manufacturers

The Brief

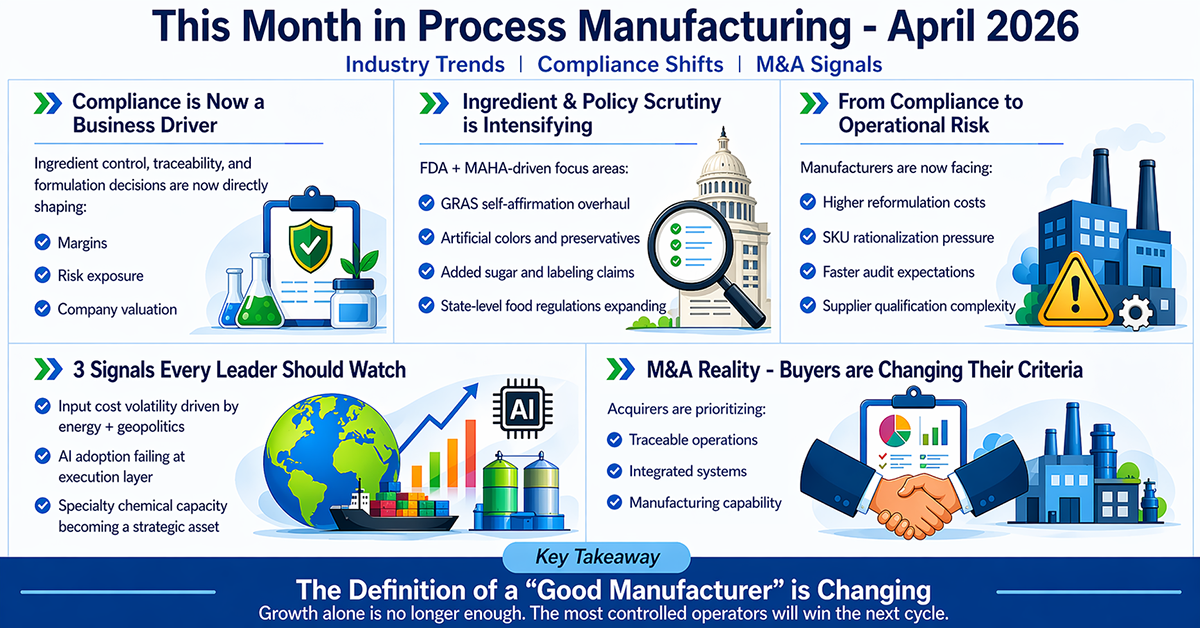

April made one shift unmistakably clear: compliance and formulation control are no longer back-office functions — they are now core drivers of margin, risk, and valuation.

Across food, beverage, nutraceutical, and chemical manufacturing, regulatory pressure is converging with cost volatility and buyer expectations. Ingredient scrutiny is intensifying; traceability requirements are expanding, and acquirers are increasingly prioritizing operational maturity over growth narratives.

For a $5M–$200M manufacturer, this changes the operating model. Reformulation cycles are accelerating; audit readiness is becoming continuous rather than episodic, and margin stability now depends on how quickly teams can respond to both regulatory shifts and input cost changes.

The leadership implication is direct: The companies that win in this environment will not be the fastest growers — they will be the most controlled operators.

Compliance & Regulatory Watch

MAHA & Ingredient Policy — From Policy to Plant-Level Impact

The most important regulatory movement this month continues to come from the FDA’s Human Foods Program under the broader MAHA agenda — and the signal is clear: ingredient oversight is tightening, and manufacturers will carry the operational burden.

FDA 2026 Human Foods Program Guidance Agenda:

The FDA’s Human Foods Program 2026 Priority Deliverables formally confirmed a series of initiatives, including:

- A proposed overhaul of the GRAS (Generally Recognized as Safe) self-affirmation framework

- Post-market reassessment of existing food chemicals

- Continued movement toward defining ultra-processed foods (UPFs)

- Ongoing development of updated labeling and formulation guidance

In parallel, the FDA launched a reassessment of BHA (Butylated Hydroxyanisole) on February 10, with public comments closing April 13, 2026 — a clear signal that legacy additives are now under active review.

Ingredients Under Scrutiny:

This month’s regulatory and policy activity consistently points to a defined set of ingredients:

- BHA and BHT (synthetic preservatives)

- Artificial food dyes (under “no artificial colors” enforcement positioning)

- Phthalates (particularly in packaging and indirect exposure pathway

- GRAS self-affirmed substances (target of structural reform)

- Added sugar levels (under FDA reduction strategy and claim positioning)

These are not theoretical risks — they represent active regulatory focus areas with downstream implications for formulation and labeling.

State-Level Patchwork:

At the same time, state-level activity continues to create complexity. California and New Jersey are advancing legislation targeting food additives and testing standards, while broader policy discussions continue around federal preemption versus state-level authority.

For manufacturers operating across multiple states, this introduces a structural challenge:

- A single formulation may not meet all regional compliance expectations

- SKU-level variation becomes increasingly likely

- Labeling consistency becomes harder to maintain

Operational & Financial Impact:

The impact here is not abstract — it is measurable:

- Reformulation costs (R&D, testing, supplier changes)

- SKU rationalization decisions (which products remain viable)

- Labeling updates and regulatory documentation

- Supplier qualification and ingredient traceability expansion

More importantly, timelines are compressing. Regulatory review cycles are shortening, while retailer and consumer expectations are moving faster than formal enforcement.

The shift is clear:

Ingredient strategy is no longer a product development decision — it is an operational risk management function.

While MAHA defines the direction of policy, traditional compliance frameworks are simultaneously becoming more demanding in execution.

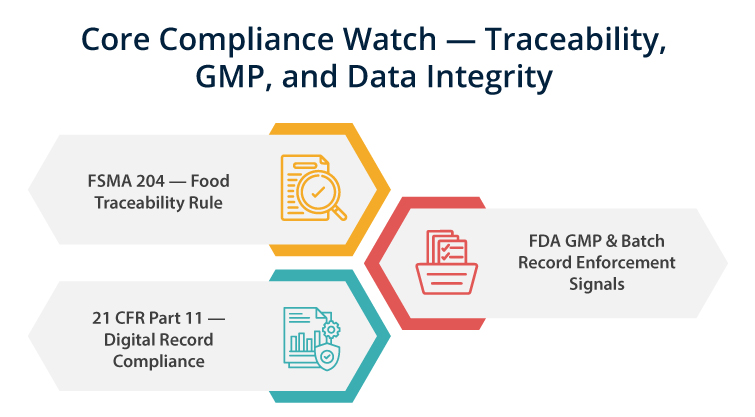

1. FSMA 204 — Food Traceability Rule

Status: Compliance date extended from January 2026 to July 2028

Applies to: Food manufacturers handling items on the Food Traceability List (FTL)

Despite the extension, enforcement expectations are not slowing down.

What’s changing operationally:

- Requirement to track Key Data Elements (KDEs) across Critical Tracking Events (CTEs)

- Expectation of rapid traceability during audits or recalls

- Increased scrutiny of record completeness and accessibility

Operational impact:

Manufacturers must move from:

- Static records → real-time traceability systems

- Batch-level visibility → lot-level and event-based tracking

The extension is not a delay — it is a preparation window.

2. FDA GMP & Batch Record Enforcement Signals

Status: Increasing inspection focus in 2026

Applies to: Food, beverage, and nutraceutical manufacturers

Regulators are placing greater emphasis on:

- Batch record completeness

- Deviation tracking and documentation

- Proof of process adherence (not just written SOPs)

Operational impact:

- Manual batch records are becoming a liability

- Audit readiness is shifting from periodic to continuous

- Data integrity and documentation accuracy are under direct scrutiny

3. 21 CFR Part 11 — Digital Record Compliance

Status: Reinforced through broader data integrity expectations

Applies to: Manufacturers using electronic records and signatures

What’s changing:

- Greater expectation of validated systems

- Traceable, secure, and tamper-evident digital records

- Alignment between production data and compliance documentation

Operational impact:

- Disconnected systems increase audit risk

- Spreadsheet-based processes become harder to defend

- Integration between production, quality, and documentation becomes critical

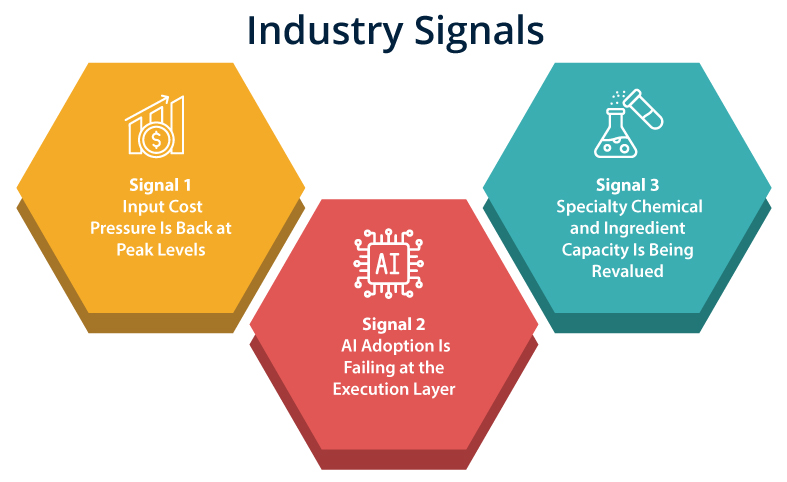

Signal 1 — Input Cost Pressure Is Back at Peak Levels

What happened:

The March 2026 ISM Report shows Manufacturing PMI at 52.7 (third consecutive month of expansion), while the Prices Paid Index surged to 78.3, its highest level since June 2022. At the same time, escalating Middle East tensions have disrupted LNG and LPG flows through key shipping routes, tightening global supply and pushing energy prices upward.

Manufacturing implication:

Cost pressure is no longer just inflation-driven — it is increasingly volatile and influenced by tariffs, geopolitical shifts, and supplier instability. Rising gas and LPG prices are now directly impacting plant utilities and feedstock costs, adding another layer of margin pressure. Static costing models and infrequent updates are no longer sufficient.

Before your next leadership meeting, ask:

Are our product-level margins accurate in real time — or are we operating on outdated cost assumptions?

Signal 2 — AI Adoption Is Failing at the Execution Layer

What happened:

Recent industry analysis shows that AI adoption in manufacturing is stalling not due to lack of investment, but due to low frontline leadership integration.

Manufacturing implication:

Technology is being introduced without embedding it into day-to-day plant operations. As a result:

- Adoption remains uneven

- Decision-making does not change

- ROI is delayed or unrealized

Before your next leadership meeting, ask:

Are new technologies changing how decisions are made on the plant floor — or just adding another layer of tools?

Signal 3 — Specialty Chemical and Ingredient Capacity Is Being Revalued

What happened:

Recent analysis shows private equity activity in chemicals shifting toward smaller, capability-driven acquisitions, with a focus on specialty formulations and domestic production.

Manufacturing implication:

Manufacturing capability — especially in complex formulations — is being treated as a strategic asset rather than a cost center.

Before your next leadership meeting, ask:

Is our manufacturing capability positioned as a cost function — or as a strategic asset that increases valuation?

M&A Intelligence

- $38.5M acquisition (Navitas Organics revenue/valuation proxy) — Laird Superfood acquired Navitas Organics (Nutraceutical / Superfood)

Laird Superfood acquired Navitas Organics for $38.5M, adding a global sourcing network, manufacturing capabilities, and organic retail distribution. The transaction was supported by a parallel $50M preferred equity raise from Nexus Capital.

Signal: Mid-market buyers are structuring deals with simultaneous capital raises, scaling both capability and financial capacity in a single move. - $28M acquisition (Farmer Brothers Coffee Co. transaction value) — Royal Cup acquired Farmer Brothers Coffee Co. (Beverage Manufacturing)

Royal Cup signed an agreement to acquire Farmer Brothers Coffee Co. in an approximately $28M all-cash transaction, combining roasting capacity, national route distribution, and equipment servicing infrastructure.

Signal: Buyers are paying for operational infrastructure and distribution scale, not brand equity. - Novopor Advanced Science (Bain Capital–backed) acquired FAR Chemical (Specialty Chemical)

Novopor Advanced Science acquired FAR Chemical to add U.S.-based manufacturing capacity in hazardous and complex specialty chemistries serving electronics, aerospace, and coatings markets.

Signal: Domestic production of complex formulations is being treated as a strategic, hard-to-build asset, not something buyers are willing to develop organically. - 1,000+ SKU expansion (combined portfolio scale) — Monterey Bay Herb Co. acquired NP Nutra (Nutraceutical Ingredients)

Monterey Bay Herb Co. acquired NP Nutra, expanding its capabilities in botanical extracts and specialty ingredients and increasing the combined portfolio to over 1,000 SKUs under a private equity–backed platform.

Signal: Buyers are consolidating ingredient sourcing, processing, and quality systems, vertically integrating capabilities that were previously fragmented.

Valuation Signal

Across April’s deal activity, one pattern stands out: buyers are prioritizing operational quality over growth narratives.

- Clean, well-documented operators continue to command premium EBITDA multiples (often 1.5x–2x higher than average peers)

- Average operators with fragmented systems and weak traceability are seeing valuation compression

What increases valuation today:

- Traceability

- Documented quality systems

- Integrated operations

What destroys it:

- Manual processes

- Inconsistent data

- Poor audit readiness

Final Takeaway

April’s signals point to a clear reality: the definition of a “good manufacturing business” is changing.

Growth alone is no longer enough. Capacity alone is no longer enough.

What matters now is:

- How controlled your operations are

- How traceable your processes are

- How adaptable your formulations are

The companies that recognize this shift early — and align operations, compliance, and systems accordingly — will not only protect margins but also position themselves for stronger valuations in an increasingly disciplined market.

CONNECT WITH US

Have insights to share? Email us at: news@batchmaster.com

Resources & Sources

MAHA & Ingredient Policy

- FDA Human Foods Program 2026 Priority Deliverables

- FDA BHA Reassessment Update (Feb–April 2026)

- MAHA Regulatory Roundup (February 2026)

- FDA Supplement Modernization & MAHA Priorities (April 8, 2026)

- FDA Added Sugar Reduction Strategy

- State-Level Food Policy & GRAS Developments

Compliance & Regulatory

- FDA Human Foods Program Guidance Agenda 2026

- FDA 2026 Regulatory Agenda Overview

- FDA 2026 Compliance Outlook

- 2026 Food Industry Regulatory Challenges

Industry Signals

- ISM Manufacturing Report — March 2026

- ISM Index Analysis — TD Economics

- Chemical Industry M&A Trends

- Food & Beverage M&A Outlook 2026

- Chemicals Deals Outlook